Bangladesh’s banking sector in global perspective: Asset quality, capital strength, and the reform agenda

- Update Time : Thursday, July 9, 2026

- 0 Time

Bangladesh’s banking sector is confronting one of the world’s most significant asset quality challenges.

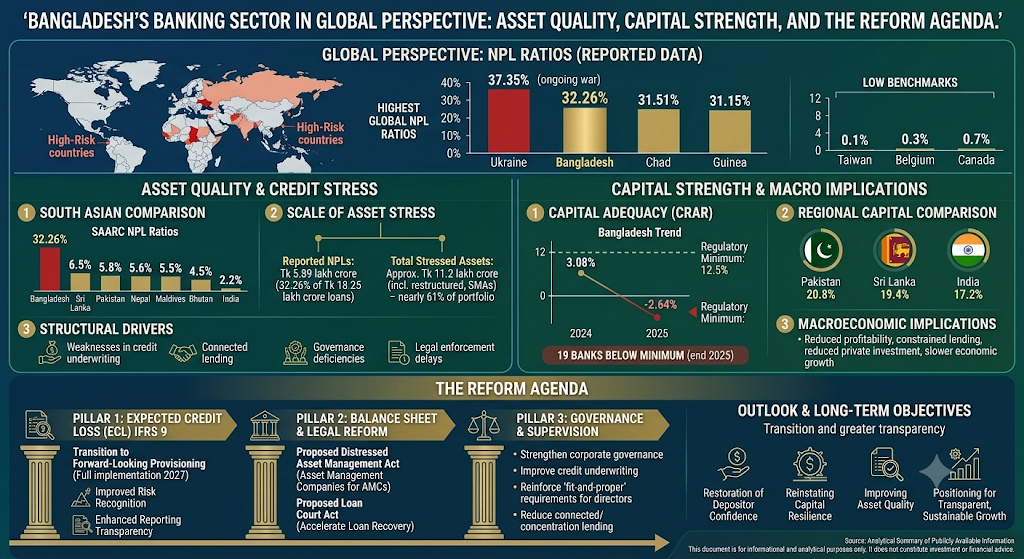

Publicly reported data indicate a non-performing loan (NPL) ratio of 32.26 percent, placing Bangladesh second globally after Ukraine, whose banking system continues to operate under the exceptional conditions of an ongoing war.

Within South Asia, Bangladesh reports the highest NPL ratio by a substantial margin.

The deterioration in asset quality has intensified concerns regarding credit discipline, capital adequacy, institutional governance, and the long-term resilience of the financial system, while prompting a broad programme of regulatory and structural reform.

Global Position

According to publicly reported international banking data, Ukraine records the world’s highest non-performing loan ratio at 37.35 percent, followed by Bangladesh at 32.26 percent. Chad and Guinea follow with reported ratios of 31.51 percent and 31.15 percent, respectively. These figures place Bangladesh among the world’s most highly stressed banking systems in terms of reported loan impairment, although the underlying economic and institutional circumstances differ across jurisdictions.

South Asian Comparison

Bangladesh reports the highest non-performing loan ratio among the member states of the South Asian Association for Regional Cooperation (SAARC). Publicly reported figures indicate NPL ratios of 32.26 percent for Bangladesh, 6.5 percent for Sri Lanka, 5.8 percent for Pakistan, 5.6 percent for Nepal, 5.5 percent for the Maldives, 4.5 percent for Bhutan, and 2.2 percent for India. The comparison highlights a markedly different credit risk profile relative to regional peers.

Scale of Asset Stress

Bangladesh Bank data cited in public reporting indicate that the banking sector held approximately Tk 18.25 lakh crore in outstanding loans, of which around Tk 5.89 lakh crore were classified as non-performing, representing an NPL ratio of 32.26 percent. When restructured loans and Special Mention Accounts are included, reported stressed assets rise to approximately Tk 11.2 lakh crore, or nearly 61 percent of the total loan portfolio, suggesting that broader credit vulnerabilities extend beyond officially classified default loans.

Capital Adequacy

The deterioration in asset quality has placed significant pressure on banking sector capital. Publicly reported Bangladesh Bank data show that the sector’s Capital to Risk-Weighted Assets Ratio (CRAR) declined from 3.08 percent at the end of 2024 to minus 2.64 percent at the end of 2025, well below the regulatory minimum requirement of 12.5 percent. The same reports indicate that 19 banks did not meet the minimum capital adequacy requirement at the end of 2025, underscoring the scale of balance sheet pressures across parts of the banking system.

Regional Capital Comparison

Bangladesh’s reported capital position compares unfavourably with several regional banking systems. Pakistan reports a Capital to Risk-Weighted Assets Ratio of 20.8 percent, Sri Lanka 19.4 percent, and India 17.2 percent. These figures indicate substantially stronger capital buffers and a greater capacity to absorb potential credit losses under adverse economic conditions.

Structural Drivers

Public policy discussions, academic research, and industry analyses have identified several factors that may contribute to elevated credit risk within Bangladesh’s banking sector. Frequently cited issues include weaknesses in credit underwriting, politically influenced lending decisions, connected lending, governance deficiencies, delayed legal enforcement, institutional capacity constraints, and information asymmetry. Research referenced in public reporting, including studies associated with Harvard Kennedy School and the Centre for International Development, similarly highlights the importance of institutional quality, regulatory effectiveness, and governance in shaping financial sector outcomes. These observations represent analytical perspectives rather than definitive findings applicable to every institution.

Macroeconomic Implications

Persistently elevated non-performing loans can reduce banking sector profitability through higher provisioning requirements, increased recovery costs, and weaker earnings. Prolonged deterioration in asset quality may also constrain new lending, weaken capital adequacy, reduce private investment, limit employment creation, and slow overall economic growth. Maintaining banking sector stability therefore remains an important prerequisite for sustainable financial intermediation and long-term economic resilience.

International Benchmarks

Several advanced banking systems continue to maintain exceptionally low levels of non-performing loans. Taiwan reports an NPL ratio of 0.1 percent, while Belgium, Sweden, and Estonia each report 0.3 percent. Norway reports 0.4 percent, and Canada 0.7 percent. These outcomes are widely associated with strong prudential supervision, disciplined credit underwriting, effective legal enforcement, robust governance, and comprehensive risk management frameworks.

Reform Agenda

Bangladesh has initiated a comprehensive programme of banking sector reforms aimed at restoring financial stability, strengthening institutional resilience, and aligning prudential regulation with internationally accepted standards. The reform agenda combines regulatory modernization, balance sheet repair, governance enhancement, and legal and judicial reforms.

A central pillar of the programme is the phased adoption of the Expected Credit Loss (ECL) framework under International Financial Reporting Standards (IFRS), with full implementation scheduled for 2027. The transition from an incurred-loss model to a forward-looking provisioning framework is intended to improve the timely recognition of credit risk, strengthen loan loss provisioning, and enhance the transparency and comparability of banks’ financial reporting.

The authorities have also announced legislative reforms, including a proposed Loan Court Act to accelerate the resolution of loan recovery cases through more efficient judicial processes. In parallel, a proposed Distressed Asset Management Act would establish the legal framework for specialized Asset Management Companies (AMCs) to acquire, manage, restructure, and recover impaired banking assets, thereby supporting balance sheet rehabilitation and improving the allocation of credit within the financial system.

Beyond these initiatives, sustained progress is expected to depend on strengthening corporate governance, enhancing supervisory effectiveness, improving credit underwriting standards, reinforcing fit-and-proper requirements for directors and senior management, reducing connected and concentration lending risks, modernizing insolvency and collateral enforcement mechanisms, strengthening internal risk management, and expanding risk-based supervision in line with international regulatory practices.

The overarching objective is to restore depositor confidence, reinforce capital resilience, improve asset quality, reduce systemic credit risk, strengthen market discipline, and position Bangladesh’s banking sector on a more transparent, sustainable, and internationally aligned foundation.

Outlook

Bangladesh’s banking sector is undergoing a period of significant transition marked by greater transparency in loan classification, enhanced recognition of credit risk, and the implementation of wide-ranging structural reforms. The long-term effectiveness of these initiatives will depend on consistent policy implementation, stronger institutional governance, improved judicial efficiency, disciplined risk management, adequate capitalization, and sustained regulatory oversight. Progress in these areas will be central to strengthening financial stability, restoring confidence in the banking system, and supporting Bangladesh’s long-term economic development.